Pay Off a 25-Year Loan in Just 10 Years

Paying off a 25-year loan in just 10 years without putting yourself under any financial stress, sound like a dream, right?. But trust me, it’s not.

With the right strategy, and financial discipline, it’s completely doable.

You are playing the game wrong!, no matter the type of loan, debt can feel suffocating. Once you understand the math behind loans you realize that every loan structure favors the banks. You keep paying EMI after EMI, but the principal it’s hardly reduced.

In this blog, I’ll walk you through:

- How EMIs actually work (spoiler: the interest trap is real),

- How the loan tenure impacts total interest paid,

- And finally, how to shorten a 25-year loan to just 10 years, without feeling like you’re drowning.

The Truth About Your EMI

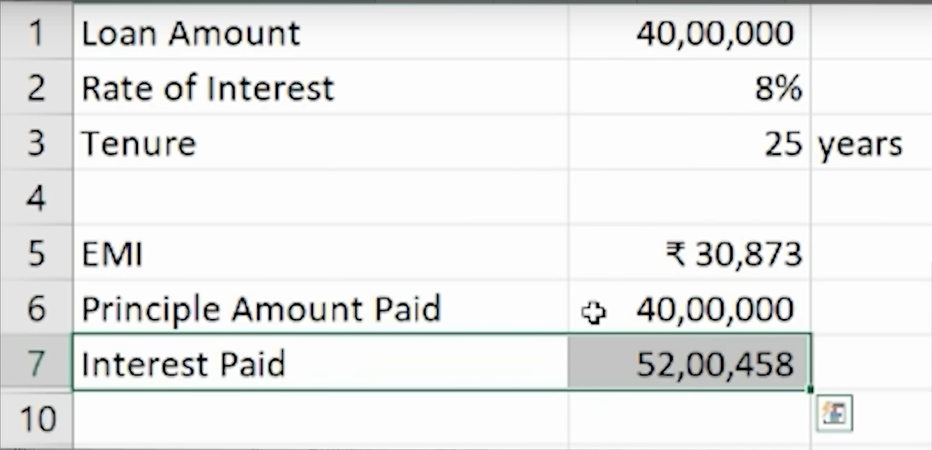

Let’s say you take a ₹40 lakh home loan at 8% interest for 25 years. Your EMI will be around ₹31,000 per month.

Now here’s the shocker: Over 25 years, you won’t just repay ₹40 lakh. You’ll end up paying around ₹92 lakh in total, ₹52 lakh just in interest!

Why? Because in the early years, more than 85% of your EMI goes toward interest, not the loan principal.

In your first EMI of ₹31,000, only about ₹4,000 goes toward reducing your loan, and the rest₹27,000, goes straight into the bank’s pocket as interest. Even after paying EMIs for a full year (₹3.7 lakh), your loan reduces by just ₹52,000.

Let that sink in.

Over time, this ratio starts to shift, but only after 12-15 years do you start paying more principal than interest. That’s how banks make their money, and how borrowers get trapped.

Shorter Tenure = Massive Savings

If you reduce your loan tenure at the very start, the interest savings can be massive.

Example:

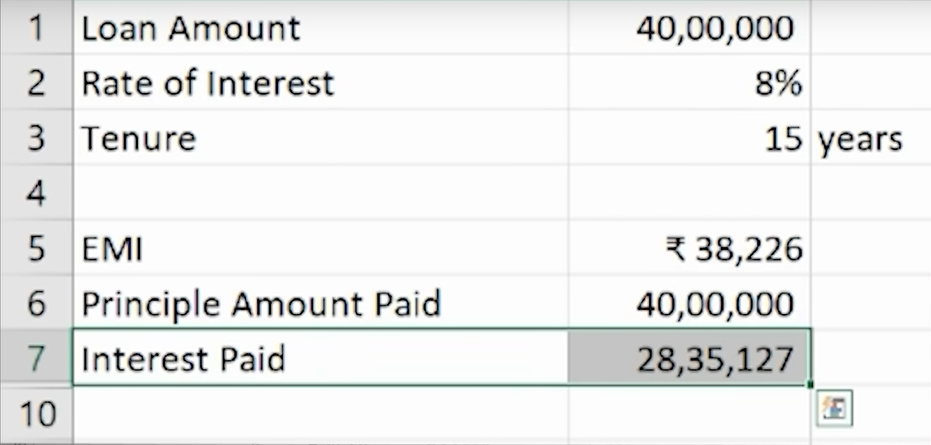

- ₹40 lakh loan for 25 years at 8% → ₹52 lakh interest

- Same loan for 15 years → ₹28 lakh interest

That’s a ₹24 lakh saving just by choosing a shorter tenure. Sure, the EMI jumps from ₹31,000 to ₹39,000. But if you can stretch a bit, you’re not just repaying faster, you’re buying your freedom a decade earlier.

But You’ve Already Taken a 25-Year Loan. Now What?

Don’t worry. Even if you’ve taken a 25-year loan, you can still hack the system using two smart strategies:

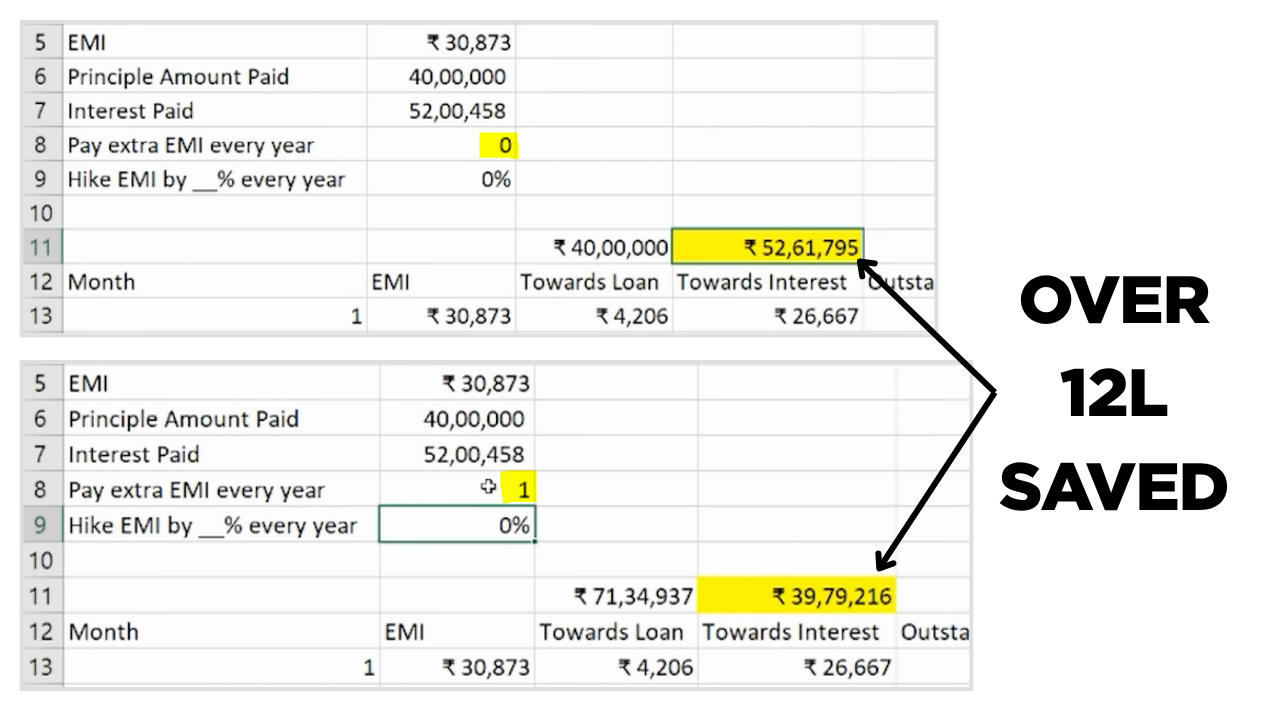

Strategy 1: Pay One Extra EMI Every Year

This is the simplest, most effective trick in the book.

Let’s say your regular EMI is ₹31,000. At the end of every year, you pay one additional EMI, that’s just ₹31,000 more for the whole year.

Just that one action brings down your total interest from ₹52 lakh to ₹40 lakh, saving you ₹12 lakh.

Do this every year, and your loan tenure drops from 25 years to about 20 years.

If you manage to pay two extra EMIs per year, your loan is done in 16 years. And the best part? This lump sum goes entirely toward the principal. No interest. That’s power.

Strategy 2: Increase Your EMI by 5–10% Every Year

Let’s face it, your income grows over time. Promotions, bonuses, side hustles, your earning power increases. Use that to your advantage.

If you increase your EMI by just 5% every year, you end up saving ₹22 lakh in interest and close your loan in just 13.5 years.

If you go bold and increase it by 10% yearly, the loan wraps up in 10 years and 5 months.

Even starting with ₹31,000 and increasing to ₹34,000 the next year, then ₹37,000, then ₹40,000, the difference is manageable, but the impact is huge.

The Super Combo: One Extra EMI + 5% Annual Hike

Let’s combine both strategies. If you:

✅ Pay one extra EMI every year

✅ Increase your EMI by 5% annually

You’ll be shocked. Your 25-year loan will be gone in just 12.5 years. That’s half the time, with over 50% savings on interest.

Now let’s up the ante…

What If It’s a ₹1 Crore Loan?

Doesn’t matter. Whether it’s ₹40 lakh or ₹1 crore, the math remains the same. The structure is proportional.

If you increase your EMI by 5% annually and make just one extra EMI payment each year, your ₹1 crore loan will also be over in just 12.5 years, saving you ₹65–70 lakh in interest.

Final Thoughts: Discipline Pays More Than Income

The secret isn’t earning more. It’s managing better. When you:

- Understand how EMI structures work,

- Choose shorter loan tenures,

- Pre-pay just one EMI extra per year,

- And increase your EMI by 5–10% annually,

You slash your loan term, save lakhs in interest, and reclaim your financial freedom.

“Compound interest is the eighth wonder of the world. He who understands it, earns it… he who doesn’t, pays it.” — Albert Einstein

Don’t just work for money. Make your money work for you.

Because this is… How Money Works

Everything I discussed in this article is what I learned from a video from Ankur Warikoo. I will encourage you to go and check his video on YouTube